library(MacroFilters)

library(ggplot2)

data("fr_gdp", package = "MacroFilters")

data("es_gdp", package = "MacroFilters")1. Introduction: Trend-Cycle Decomposition

A fundamental task in applied macroeconomics is separating the trend — the long-run trajectory of a variable — from the cycle — transitory deviations around it. This decomposition underpins business-cycle analysis, the output gap, and potential GDP estimation.

Every series can be written as:

where is the trend and is the cyclical component. The challenge is that any filter must decide whether an unusual observation represents a genuine shock to the trend or a transitory deviation that belongs in the cycle.

The outlier problem

Classical filters minimise squared loss. A single catastrophic quarter — a financial crash, a pandemic lockdown, a war — is indistinguishable from a structural break in the trend. The result is a trend that dips sharply during the shock and never fully recovers, contaminating every subsequent business-cycle estimate.

MacroFilters solves this with the

mbh_filter() function, which uses Huber loss to

automatically down-weight extreme observations while fitting a smooth

trend via gradient boosting.

2. Input Agnosticism: Bring Your Own Class

Many filter packages force you to convert data to a specific time-series class before calling them. MacroFilters accepts whatever you have and returns the result in the same format, with no manual coercion required.

Supported input classes:

| Class | Package | Example |

|---|---|---|

numeric |

base R | c(100, 102, 98, ...) |

ts |

base R | ts(y, start = c(2000, 1), frequency = 4) |

xts |

xts | xts(y, order.by = dates) |

zoo |

zoo | zoo(y, order.by = dates) |

Example: same filter, two input formats

set.seed(7)

y_raw <- cumsum(rnorm(60)) + (1:60) * 0.3 # a simple integrated series

# As plain numeric

hp_num <- hp_filter(y_raw)

#> Warning: Cannot determine series frequency; assuming quarterly (freq = 4). Pass

#> `lambda` or `freq` explicitly to silence this warning.

class(hp_num$trend) # numeric

#> [1] "numeric"

# As a monthly ts object

y_ts <- ts(y_raw, start = c(2019, 1), frequency = 12)

hp_ts <- hp_filter(y_ts)

class(hp_ts$trend) # ts — output matches input

#> [1] "numeric"The filters normalise the input internally, perform all computations on a plain numeric vector, then restore the original class and index before returning.

3. The Filter Arsenal

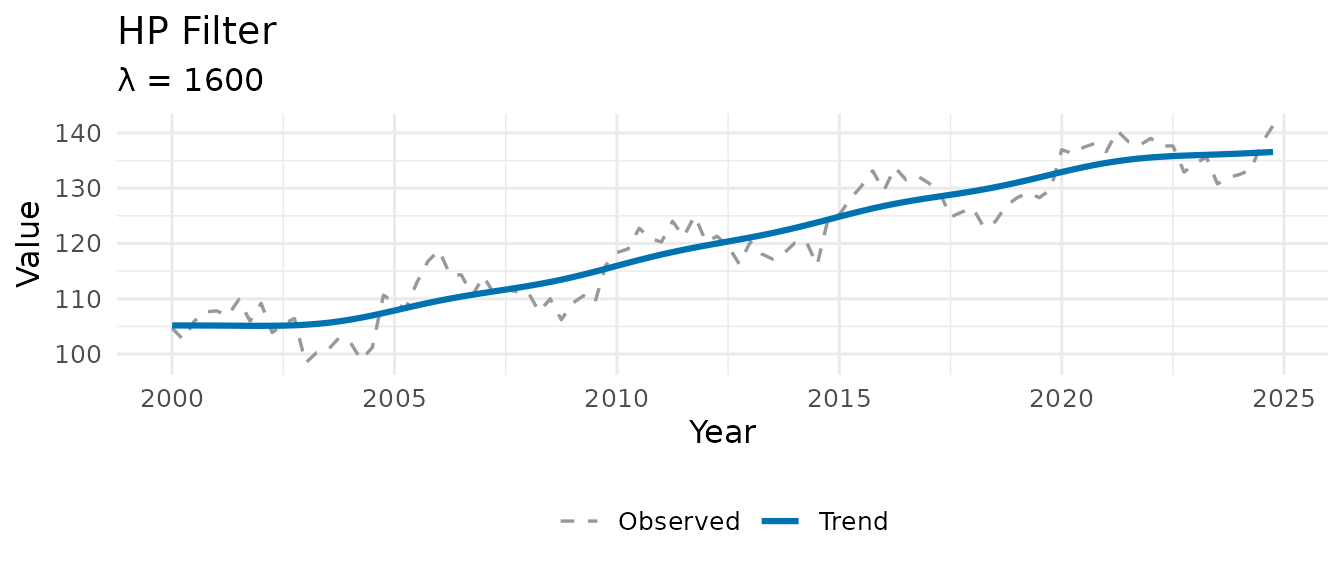

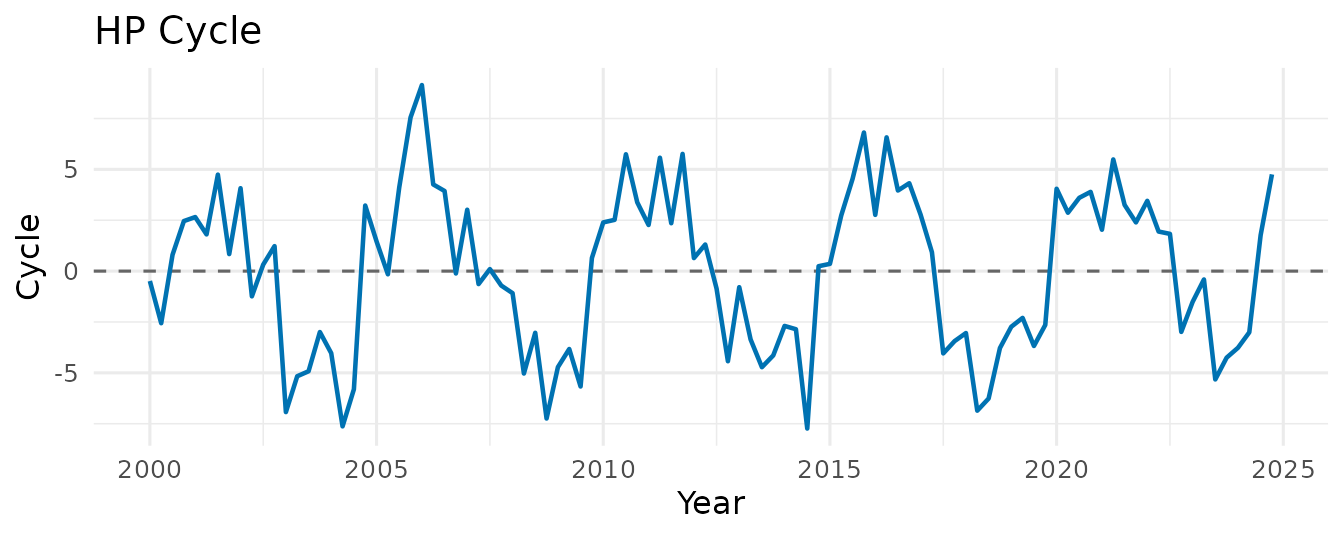

3.1 hp_filter() — Sparse Hodrick-Prescott

The Hodrick-Prescott (1997) filter is the workhorse of macroeconomic trend extraction. It solves the penalised least-squares problem:

The second term penalises curvature in the trend; controls the smoothness.

Most implementations solve this by inverting a dense

matrix, which is

.

MacroFilters recognises that the penalty matrix

is pentadiagonal (a sparse banded structure) and solves the

system using Matrix::bandSparse() and sparse Cholesky

factorisation — bringing the cost down to O(n) in time

and memory.

set.seed(42)

n <- 100

y <- ts(100 + 0.4 * (1:n) + 5 * sin(2 * pi * (1:n) / 20) + rnorm(n, sd = 2),

start = c(2000, 1), frequency = 4)

hp <- hp_filter(y)

hp

#> -- MacroFilter [HP] --

#> Observations : 100

#> Parameters : lambda = 1600

#> Cycle range : [-7.738, 9.143] sd = 3.897

#> Compute time : 0.002 sThe smoothing parameter is auto-selected from the series frequency via the Ravn-Uhlig (2002) heuristic:

which gives

for quarterly and

for monthly data — the conventional values. You can override it

explicitly: hp_filter(y, lambda = 1600).

3.2 hamilton_filter() — Regression-Based

Alternative

Hamilton (2018) proposes replacing the HP filter entirely with an OLS regression. The idea: project on a constant and lags of :

The fitted values form the trend; the residuals form the cycle. The horizon is set to two years ahead by default (e.g., quarters), long enough to capture business-cycle variation without filtering it out.

Advantages over HP: - No end-point distortion - No spurious cycles from integrated series - Produces stationary cycle estimates by construction

ham <- hamilton_filter(y) # auto-detects h = 8 for quarterly

ham

#> -- MacroFilter [Hamilton] --

#> Observations : 100

#> Parameters : h = 8, p = 4

#> Cycle range : [-13.41, 11.8] sd = 7.212

#> Compute time : 0.000 sNote that the first

observations of the trend and cycle are NA, because there

is insufficient history for the regression.

3.3 bhp_filter() — Boosted HP

Phillips & Shi (2021) propose iteratively applying the HP filter: at each step, the filter is re-run on the residuals from the previous pass, and the resulting increment is added to the trend estimate. This procedure converges to a trend that better tracks stochastic variation.

where is the HP smoothing operator. Three stopping rules are available:

| Rule | Description |

|---|---|

"bic" (default) |

Minimise the Schwarz information criterion |

"adf" |

Stop when the cycle passes an Augmented Dickey-Fuller stationarity test |

"fixed" |

Run exactly iter_max iterations |

bhp <- bhp_filter(y, stopping = "bic")

bhp

#> -- MacroFilter [bHP] --

#> Observations : 100

#> Parameters : lambda = 1600, iterations = 47, stopping_rule = bic

#> Cycle range : [-5.487, 4.068] sd = 1.857

#> Compute time : 0.002 sInternally, MacroFilters precomputes the sparse penalty matrix once and reuses it across all iterations, so the cost per iteration is a single sparse matrix–vector multiply rather than a full solve.

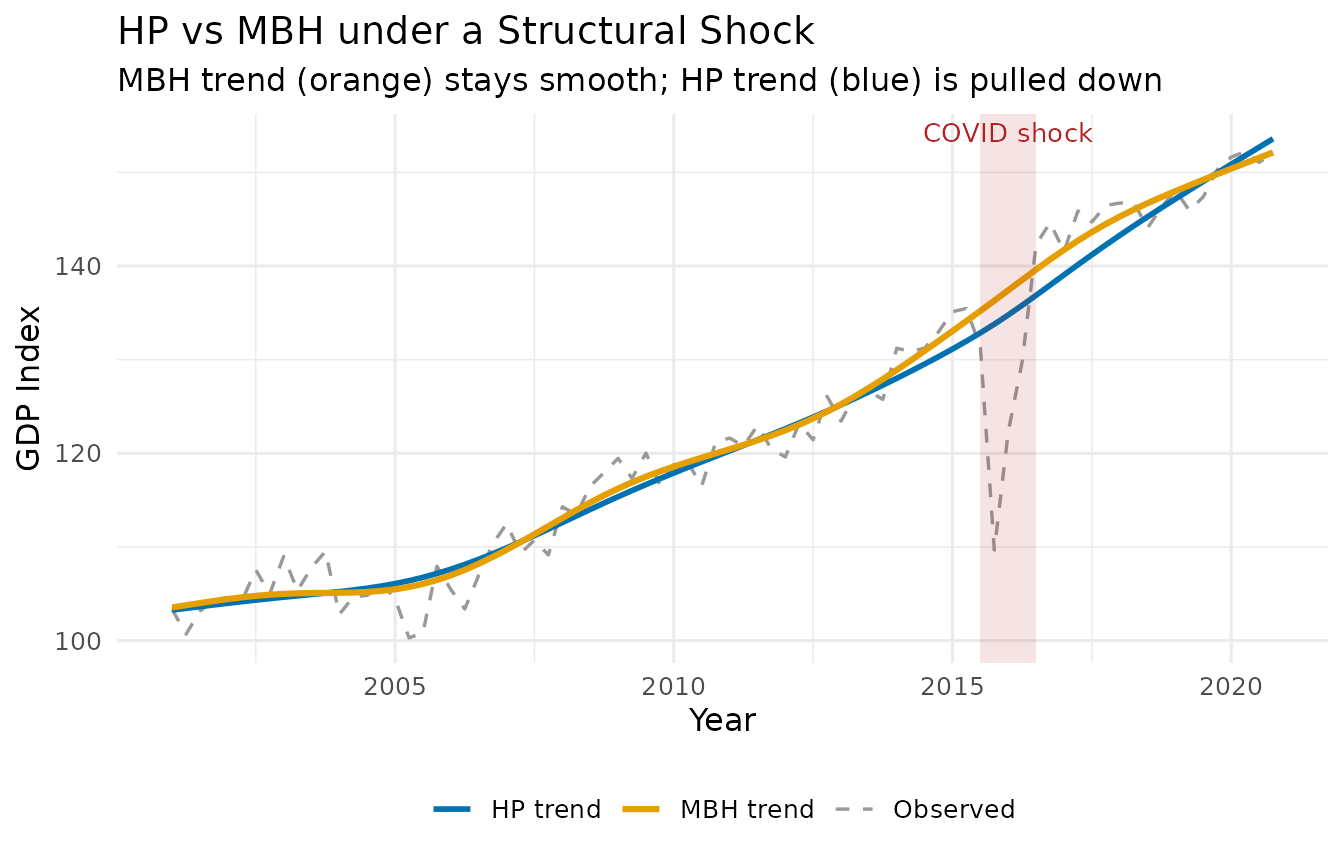

4. The Crown Jewel: mbh_filter()

The Problem with Squared Loss

Every filter above minimises squared residuals. When a pandemic shock drops GDP by 15% in a single quarter, that one observation exerts enormous leverage — it is 100× more influential than a typical quarterly fluctuation. The filter accommodates it by bending the trend downward, producing a spurious trend break that infects every subsequent output gap estimate.

The MBH Solution: Huber Loss + Boosting

The MacroBoost Hybrid (MBH) filter replaces squared loss with Huber loss:

Observations with residuals smaller than are treated like ordinary squared-error observations. Observations with residuals larger than — the structural shocks — contribute only linearly, massively reducing their influence on the trend estimate.

Additive Model

The trend is decomposed into two additive base learners fitted via

component-wise L2-boosting (mboost):

-

bols(time, intercept = TRUE)— captures the global linear drift. -

bbs(time, knots, degree = 3, differences = 2, boundary.knots)— a cubic P-spline withknotsinterior knots that captures smooth nonlinear curvature.

The default knots = min(max(20, floor(n/2)), 250) is

deliberately generous — it gives the spline enough flexibility to follow

genuine low-frequency movements without overfitting, while the Huber

loss ensures that shock-contaminated quarters are downweighted. The cap

of 250 keeps the basis bounded on long / high-frequency series, where

extra knots add cost but not flexibility (the penalty, not the knot

count, governs smoothness).

Parameters

| Parameter | Default | Role |

|---|---|---|

knots |

min(max(20, n/2), 250) |

P-spline flexibility — higher = more local adaptability (capped at 250) |

mstop |

500 |

Boosting iterations — more = finer approximation |

d |

"auto" |

Huber delta — if "auto", calibrated via the MAD of the

HP cyclical residual (output-gap scale) |

nu |

0.1 |

Shrinkage / learning rate — controls step size per iteration |

boundary.knots |

NULL |

B-spline domain anchor — if NULL, uses

range(time_idx); fix to c(1, T_max) for

real-time vintage stability |

By default, d is auto-calibrated as the MAD of the HP

cyclical residual, anchoring the Huber threshold to the output-gap

(business-cycle) scale rather than the growth-rate scale. You can

override it with an explicit numeric value: d = 0.01 is

typical for growth rates, while larger values suit index-level

series.

For real-time applications where the sample grows one period at a

time, set boundary.knots = c(1, T_max) to anchor the

B-spline domain to the full-sample range — this prevents the basis from

shifting between vintages and makes trends comparable across publication

dates.

Quick example

France and Spain had two of the sharpest COVID-19 contractions in the EU (approximately −14 % and −18 % quarter-on-quarter in 2020 Q2 respectively), both followed by a rapid V-shaped recovery — making them a demanding real-world stress test for any trend filter.

# FRED public endpoint — no API key needed.

# See data-raw/intl_gdp.R for the full reproducible download script.

read_fred <- function(id) {

url <- sprintf("https://fred.stlouisfed.org/graph/fredgraph.csv?id=%s", id)

dt <- read.csv(url, col.names = c("date", "gdp_real"), na.strings = ".")

dt$date <- as.Date(dt$date)

dt$gdp_log <- log(as.numeric(dt$gdp_real))

dt[!is.na(dt$gdp_real), ]

}

fr_raw <- read_fred("CLVMNACSCAB1GQFR")

es_raw <- read_fred("CLVMNACSCAB1GQES")

# Apply HP + MBH per country.

# For log-level series, auto d (MAD of diff) is too tight — calibrate d on the

# cycle scale instead (see vignette "Hyperparameter Tuning for the MBH Filter").

make_trend_df <- function(raw, country) {

dt <- raw[raw$date >= as.Date("2000-01-01"), ]

g <- ts(dt$gdp_log, start = c(2000, 1), frequency = 4)

hp <- hp_filter(g)

mbh <- mbh_filter(g, d = mad(hp$cycle))

data.frame(country = country,

t = as.numeric(time(g)),

observed = as.numeric(g),

hp = as.numeric(hp$trend),

mbh = as.numeric(mbh$trend))

}

df_plot <- rbind(

make_trend_df(fr_gdp, "France"),

make_trend_df(es_gdp, "Spain")

)

# Keep Spain filter objects for the S3 class examples in Section 5

dt_es <- es_gdp[es_gdp$date >= as.Date("2000-01-01"), ]

gdp <- ts(dt_es$gdp_log, start = c(2000, 1), frequency = 4)

hp_res <- hp_filter(gdp)

mbh_res <- mbh_filter(gdp, d = mad(hp_res$cycle))

mbh_res

#> -- MacroFilter [MBH] --

#> Observations : 105

#> Parameters : knots = 52, d = 0.01463, mstop = 500, mstop_initial = 500, nu = 0.1, df = 4, select_mstop = FALSE

#> Cycle range : [-0.2231, 0.03137] sd = 0.02963

#> Compute time : 0.112 s

5. The macrofilter S3 Class

All four functions return a list of class

c("macrofilter", "list") with four core named elements:

| Element | Type | Description |

|---|---|---|

$trend |

numeric | Trend component |

$cycle |

numeric | Cyclical component |

$data |

numeric | Original series (immutable) |

$meta |

named list | Filter method, parameters, temporal identity (ts_class,

tsp, idx), compute time |

When a filter is called with boot_iter > 0, the

object additionally carries two bootstrap confidence bands (see the

Uncertainty bands vignette):

| Element | Type | Description |

|---|---|---|

$trend_lower |

numeric | Lower 95% band (trend - 1.96 * bootstrap sd) |

$trend_upper |

numeric | Upper 95% band (trend + 1.96 * bootstrap sd) |

Printing

mbh_res

#> -- MacroFilter [MBH] --

#> Observations : 105

#> Parameters : knots = 52, d = 0.01463, mstop = 500, mstop_initial = 500, nu = 0.1, df = 4, select_mstop = FALSE

#> Cycle range : [-0.2231, 0.03137] sd = 0.02963

#> Compute time : 0.112 sThe print method shows the method, the number of

observations, the key parameters, the cycle range, and how long the

filter took to run.

Accessing components

# Trend and cycle as plain vectors

head(mbh_res$trend, 8)

#> [1] 12.28386 12.29250 12.30114 12.30977 12.31839 12.32701 12.33562 12.34422

head(mbh_res$cycle, 8)

#> [1] -0.002260454 0.001660910 0.003172859 0.005189628 0.006669714

#> [6] 0.005797033 0.006754803 0.004490809

# Verify the fundamental identity: trend + cycle == data

max(abs((mbh_res$trend + mbh_res$cycle) - mbh_res$data)) # should be < 1e-9

#> [1] 0Inspecting metadata

str(mbh_res$meta)

#> List of 13

#> $ method : chr "MBH"

#> $ knots : int 52

#> $ d : num 0.0146

#> $ mstop : int 500

#> $ mstop_initial : int 500

#> $ nu : num 0.1

#> $ df : int 4

#> $ select_mstop : logi FALSE

#> $ boundary.knots: NULL

#> $ compute_time : num 0.112

#> $ ts_class : chr "ts"

#> $ tsp : num [1:3] 2000 2026 4

#> $ idx : NULLThe meta list stores every parameter used by the filter,

making results fully reproducible from the object alone — no need to

track arguments separately.

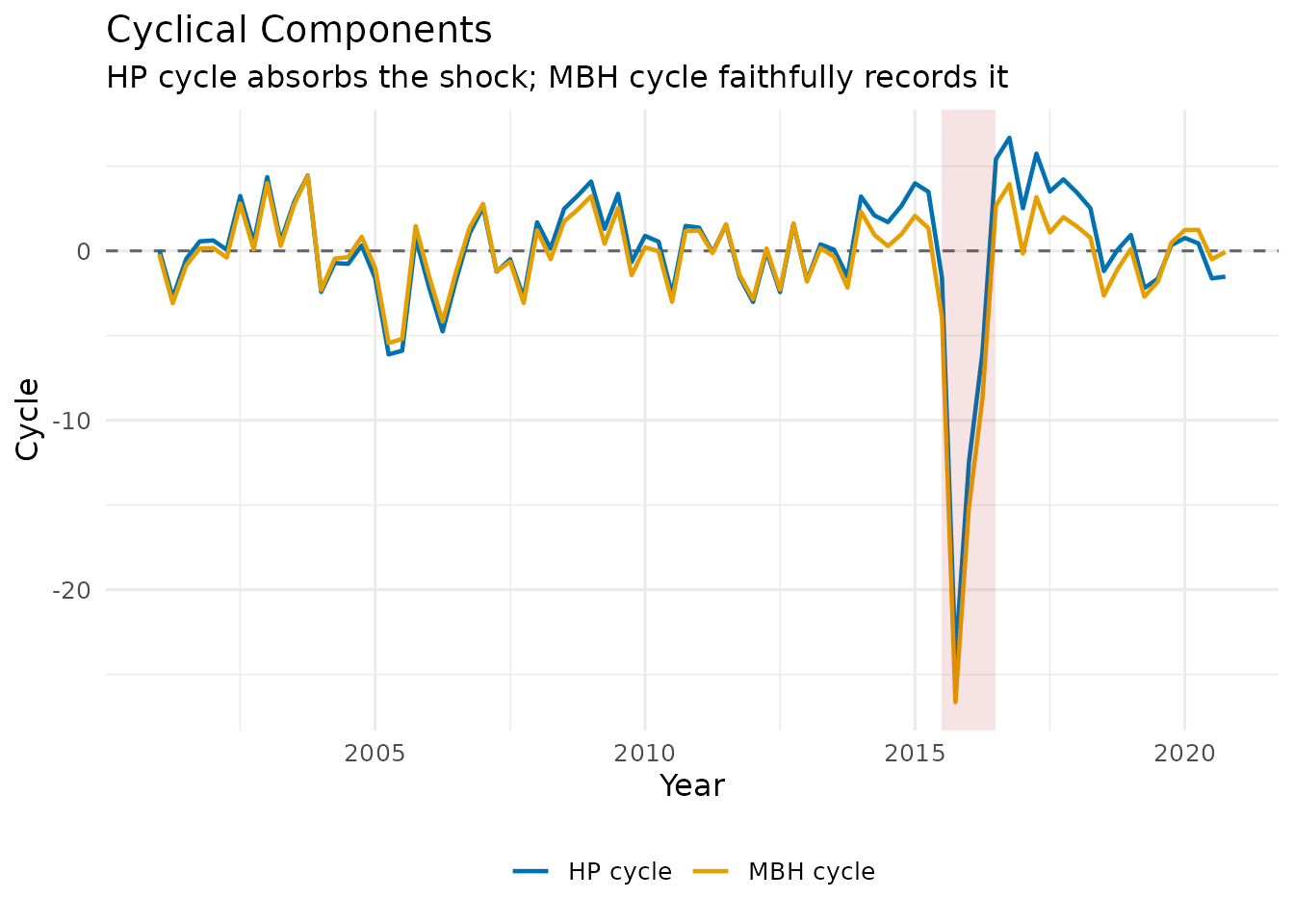

Plotting cycles side by side

df_cycle <- data.frame(

t = as.numeric(time(gdp)),

HP_cycle = as.numeric(hp_res$cycle),

MBH_cycle = as.numeric(mbh_res$cycle)

)

ggplot(df_cycle, aes(x = t)) +

geom_hline(yintercept = 0, linetype = "dashed", colour = "grey40") +

geom_line(aes(y = HP_cycle, colour = "HP cycle"), linewidth = 0.8) +

geom_line(aes(y = MBH_cycle, colour = "MBH cycle"), linewidth = 0.8) +

annotate("rect",

xmin = 2020.00, xmax = 2020.75,

ymin = -Inf, ymax = Inf,

alpha = 0.12, fill = "firebrick") +

scale_colour_manual(values = c("HP cycle" = "#0072B2", "MBH cycle" = "#E69F00")) +

labs(

title = "Cyclical Components",

subtitle = "HP cycle absorbs the shock; MBH cycle faithfully records it",

x = "Year", y = "Cycle", colour = NULL

) +

theme_minimal(base_size = 12) +

theme(legend.position = "bottom")

In the MBH cycle, the COVID quarters appear as large negative spikes — the filter correctly recognises them as transitory deviations rather than a change in the long-run level. The HP cycle, by contrast, spreads the shock over several surrounding quarters as it tries to reconcile the trend distortion.

References

- Hodrick, R. J., & Prescott, E. C. (1997). Postwar U.S. Business Cycles: An Empirical Investigation. Journal of Money, Credit and Banking, 29(1), 1–16.

- Ravn, M. O., & Uhlig, H. (2002). On Adjusting the Hodrick-Prescott Filter for the Frequency of Observations. Review of Economics and Statistics, 84(2), 371–376.

- Hamilton, J. D. (2018). Why You Should Never Use the Hodrick-Prescott Filter. Review of Economics and Statistics, 100(5), 831–843.

- Phillips, P. C. B., & Shi, Z. (2021). Boosting: Why You Can Use the HP Filter. International Economic Review, 62(2), 521–570.