Working Paper Available: The econometric methodology and mathematical proofs underlying this package are distributed via SSRN: Robust Real-Time Macroeconomic Trend Extraction: A Gradient Boosting Approach.

MacroFilters is a unified, high-performance library for extracting trend and cycle components from macroeconomic time series. It combines classical filters (Hodrick-Prescott, Hamilton, Boosted HP) with its flagship algorithm, the MacroBoost Hybrid (MBH) — a gradient-boosting filter with Huber loss that is immune to structural shocks such as COVID-19, financial crises, and wars.

Why MacroFilters instead of mFilter or neverhpfilter?

-

Robustness:

mbh_filter()replaces squared-error loss with Huber loss, ensuring extreme exogenous shocks never distort the structural trend. -

Speed: The HP implementation uses sparse-matrix Cholesky factorisation (

Matrix), scaling as O(n) instead of the dense O(n³) used by legacy packages. -

Input agnosticism: Pass a plain

numericvector, ats, anxts, or azooobject — the output always matches the input class seamlessly.

The End-Point Problem: Solved

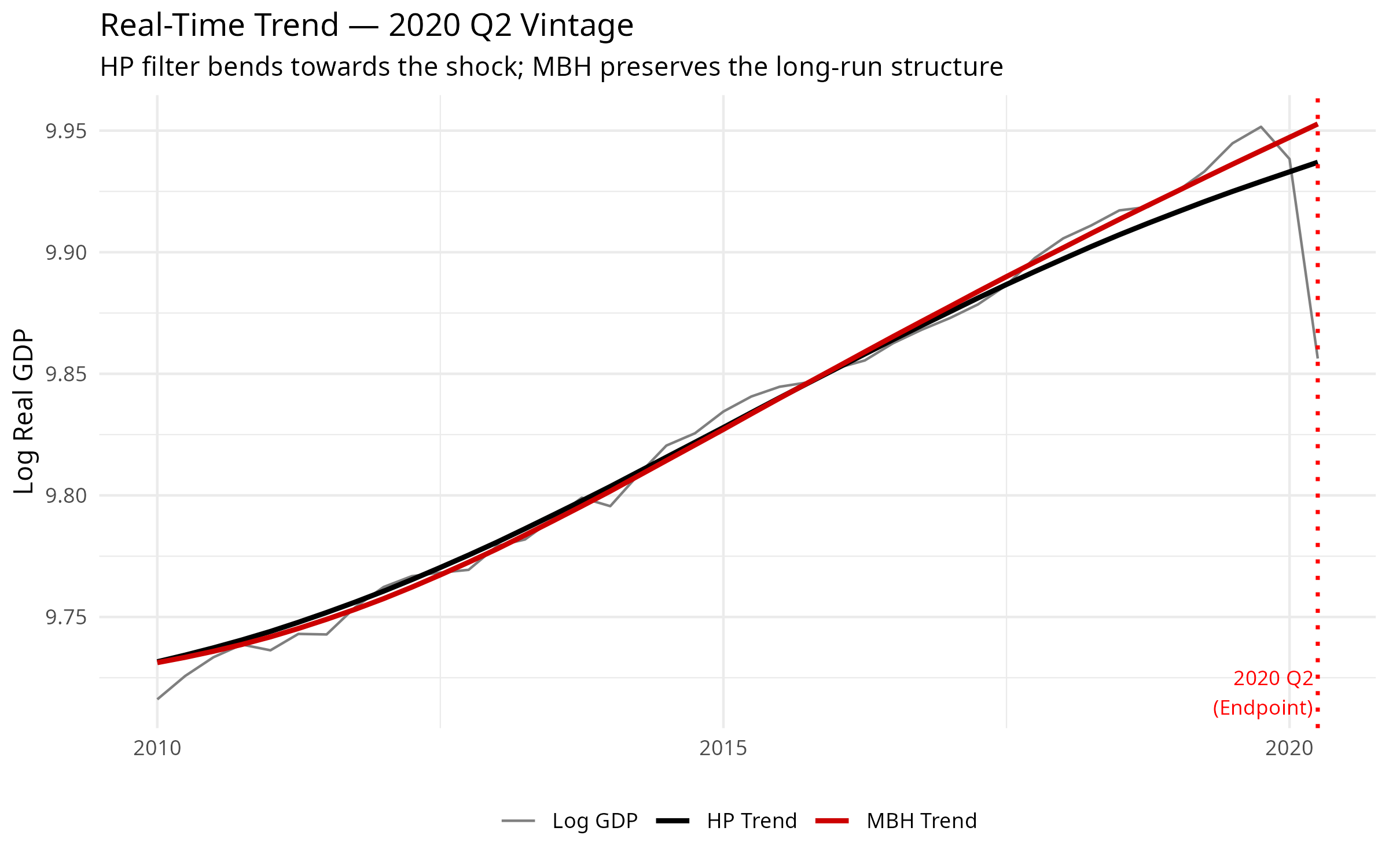

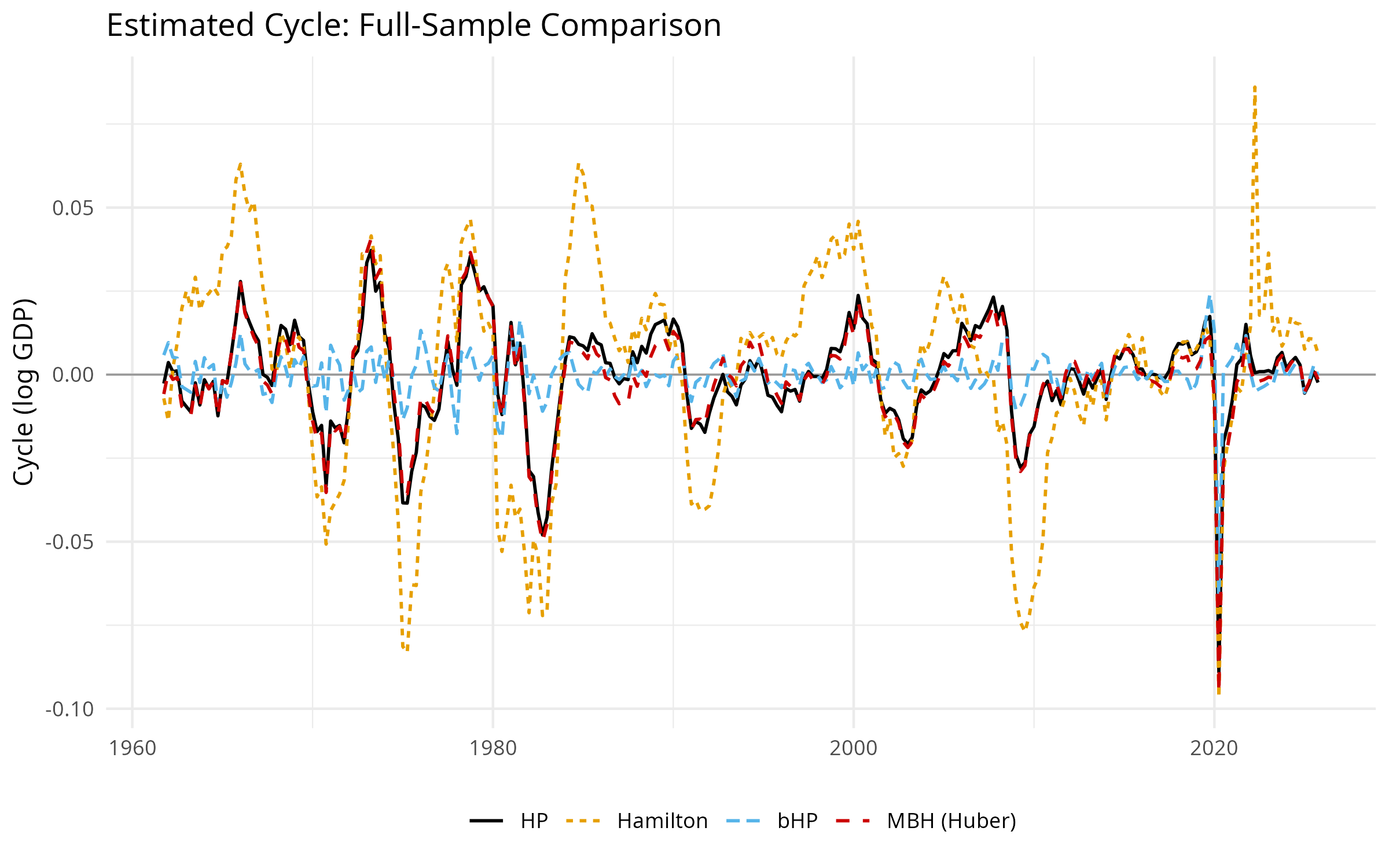

During extreme black swan events, traditional filters anchored in loss mechanically deform the long-run structural trend to absorb massive, transitory outliers.

As demonstrated with Real US GDP during the 2020 Q2 COVID-19 collapse, the standard HP filter bends towards the shock. The MBH filter isolates the exogenous shock entirely within the cyclical component, preserving absolute trend integrity in real-time.

Furthermore, ex-ante spectral alignment ensures the MBH filter perfectly matches the baseline cyclical volatility of the industry-standard HP filter during normal conditions, unlike the excessively volatile Hamilton filter.

(Plots generated using real-time vintage data from the Federal Reserve Economic Data - FRED).

Quick Start Arsenal

| Function | Method | Key Advantage |

|---|---|---|

hp_filter() |

Hodrick-Prescott (1997) | Sparse O(n) implementation |

hamilton_filter() |

Hamilton (2018) | OLS regression, no spurious cycles |

bhp_filter() |

Boosted HP — Phillips & Shi (2021) | Iterative fitting with BIC/ADF stopping |

mbh_filter() |

MacroBoost Hybrid | Robust to outliers via Huber loss |

All functions return a list of class c("macrofilter", "list").

library(MacroFilters)

# Fast, agnostic filtering on any time-series object

hp_result <- hp_filter(us_gdp_xts)

mbh_result <- mbh_filter(us_gdp_xts)

# Access components directly

mbh_result$trend

mbh_result$cycle

# Add 95% bootstrap confidence bands and plot them

mbh_ci <- mbh_filter(us_gdp_xts, boot_iter = 50L)

autoplot(mbh_ci) # ggplot: trend, observed series and confidence ribbonFurther Reading

-

vignette("introduction", package = "MacroFilters")— full walkthrough of all four filters and the S3 print/meta interface. -

vignette("uncertainty_bands", package = "MacroFilters")— confidence bands via block bootstrap and theautoplot()method.